CFO Mindset 2.0

Navigating the finance software maze, and how to find the middle ground.

Table of contents

Methodology

The findings in the 2025 CFO Mindset report are based on a survey of 1,000 senior finance professionals, comprising Chief Financial Officers, Heads of Finance, Financial Controllers and Finance Directors. Of these, 800 respondents were based in the United Kingdom and 200 in Ireland.

All participants represented organisations employing between 20 and 250 staff, across a range of sectors including technology, private equity, hospitality, law, and professional services.

The survey was conducted between June and July 2025.

Senior finance professionals

Based in the UK

Based in Ireland

Executive summary

Regret is a common thread, even at the highest levels of financial leadership.

According to our latest CFO Mindset survey, 94% of finance leaders admit to making a strategic decision about software they now regret due to time, cost and stress implications. In this report, we examine what’s driving those decisions — and how to avoid repeating them.

A year on from our inaugural CFO Mindset report, the role of the CFO has continued to evolve, with finance leaders making more of an impact than ever in the boardroom. This, understandably, leads to more pressure. Pressure to battle ongoing uncertainty, to stay on top of rapidly evolving tech trends like AI, and to keep pace with competitors and drive growth.

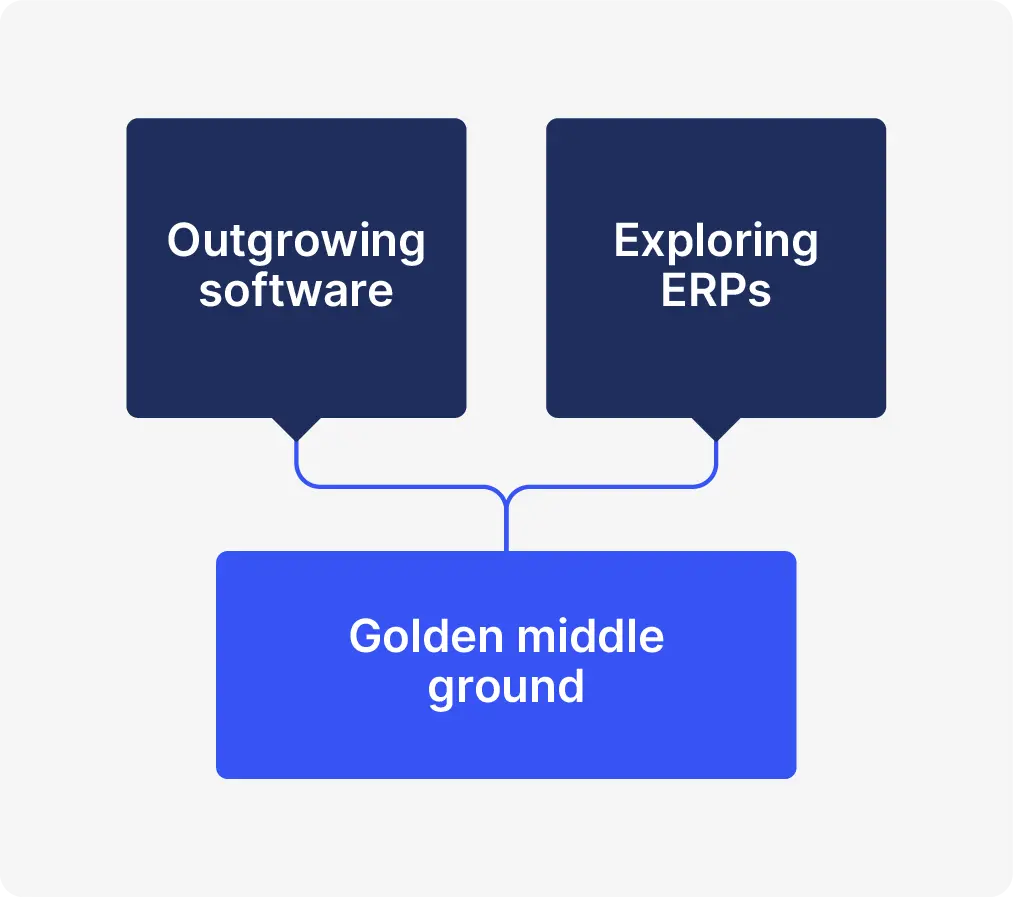

But as our research reveals, choosing the right finance platform is far easier said than done, especially for mid-sized organisations.

On one side are businesses that have quickly outgrown their starter finance software and are stuck using outdated systems. They desperately need more functionality, but are often unsure what options are out there — whether to stay with their current system or opt for an enterprise resource planning (ERP) system or another product.

On the other side are those who have implemented an ERP to match their size, needs and growth, only to realise it’s too complex and costly.

In this report, you’ll discover:

The business cost

The human cost

Breaking the cycle

What's next?

Key findings

of finance leaders regret implementing an ERP

use 50% or less of available ERP features

found the ERP implementation process stressful

have experienced hidden costs relating to their finance software

plan to switch finance systems in the next 3 months

report that financial decisions are sometimes made without enough data

Chapter 1: The business cost

Why are many software decisions ending in regret?

Why so many software decisions go wrong — and how the fallout really stacks up.

When companies grow quickly, they can reach a fork in the road with their finance software. They might have outgrown their current platform, be it Xero or Sage 50, and need more features and capabilities.

This need for greater functionality can lead to finance teams adopting more complex systems designed for large organisations — like an ERP — which they don’t actually need.

But here’s the catch: a massive 94% of finance leaders who have implemented an ERP said they regret it. That’s a striking revelation. Imagine if nearly every customer at a restaurant were to complain about their experience.

So, why are so many finance leaders having major regrets with their ERPs? Why are they not opting for software more suited to their size and needs?

Practically the same percentage (95%) also said they have encountered unexpected hidden costs with their finance software providers. It’s an incredible picture: businesses are paying premium prices for tools that slow growth, drain efficiency and burn out teams.

Phase one: The decision phase

As mid-sized businesses grow, their finance needs quickly outpace entry-level software. Frustrated by limitations, finance leaders urgently need more functionality and face a critical question: what should their next upgrade be?

The choice can feel overwhelming. Many platforms seem impressive on the surface, packed with shiny features, but the reality often disappoints. Thinking that an ERP is the only viable option, many overlook software designed specifically for mid-sized organisations. Bigger brands fuel this perception, while alternatives sometimes fly under the radar.

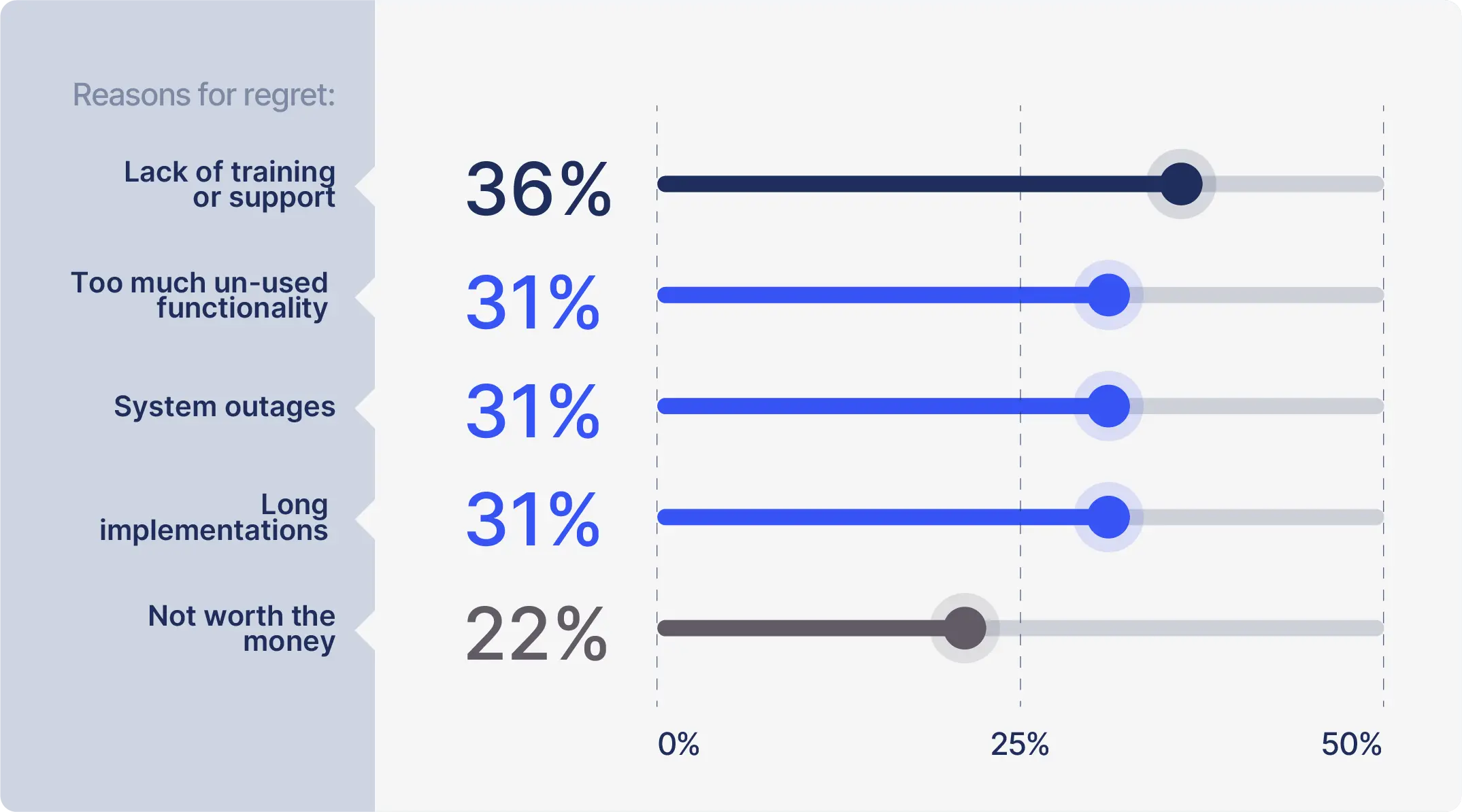

Dig deeper, and cracks appear. ERP regret is more common than you may think, with CFOs citing the following reasons:

Phase two: Implementation

The implementation phase is pivotal to how well finance software is integrated, used and perceived by finance teams. If it can be smoothly and efficiently embedded into existing finance processes, it stands a far higher chance of success.

An ideal implementation process takes between 4–6 weeks. Yet for a quarter of the leaders surveyed, it took seven months or more; that’s over half a year before fully using their new system (while still relying on the old one). A third said that it took them at least 3–6 months. In total, three in five finance leaders reported painfully slow ERP implementations.

Scenario 1

You’ve arranged a kitchen renovation and have been told it will take a month, only to find yourself eating takeaways for over half a year while you wait for the builders to finish. That’s five extra months of fees and stress of not having a kitchen without getting any value or return on investment in that timeframe.

Phase three: (Under)utilisation

On the face of it, a CFO or finance leader may have decided on a new software and completed the implementation in a relatively seamless manner. But then the real test emerges: how much is the platform used and how well does it work for the team? Crucially, was it worth the money and resources spent on introducing it to the business?

Only 2% of finance leaders said they use all of their ERP functionality. Three in five (60%) use less than half of their software’s functionality, and 87% use no more than three quarters. That’s a lot of waste.

The average ERP costs mid-sized organisations around £100,000 a year. If only half the functionality is used, that’s £50,000 effectively wasted each year. And this is happening to almost two thirds of finance teams.

Scenario 2

Imagine paying for a premium gym membership with 100 machines, every class, the pool, sauna, and courts — yet you only use a handful of machines because you never learned to swim, can’t play squash and only really see any benefit from doing strength workouts. That’s the ERP dilemma for mid-sized businesses.

Clearly, many finance leaders are overbuying functionality and underusing it. Simplicity and usability always beat endless features."

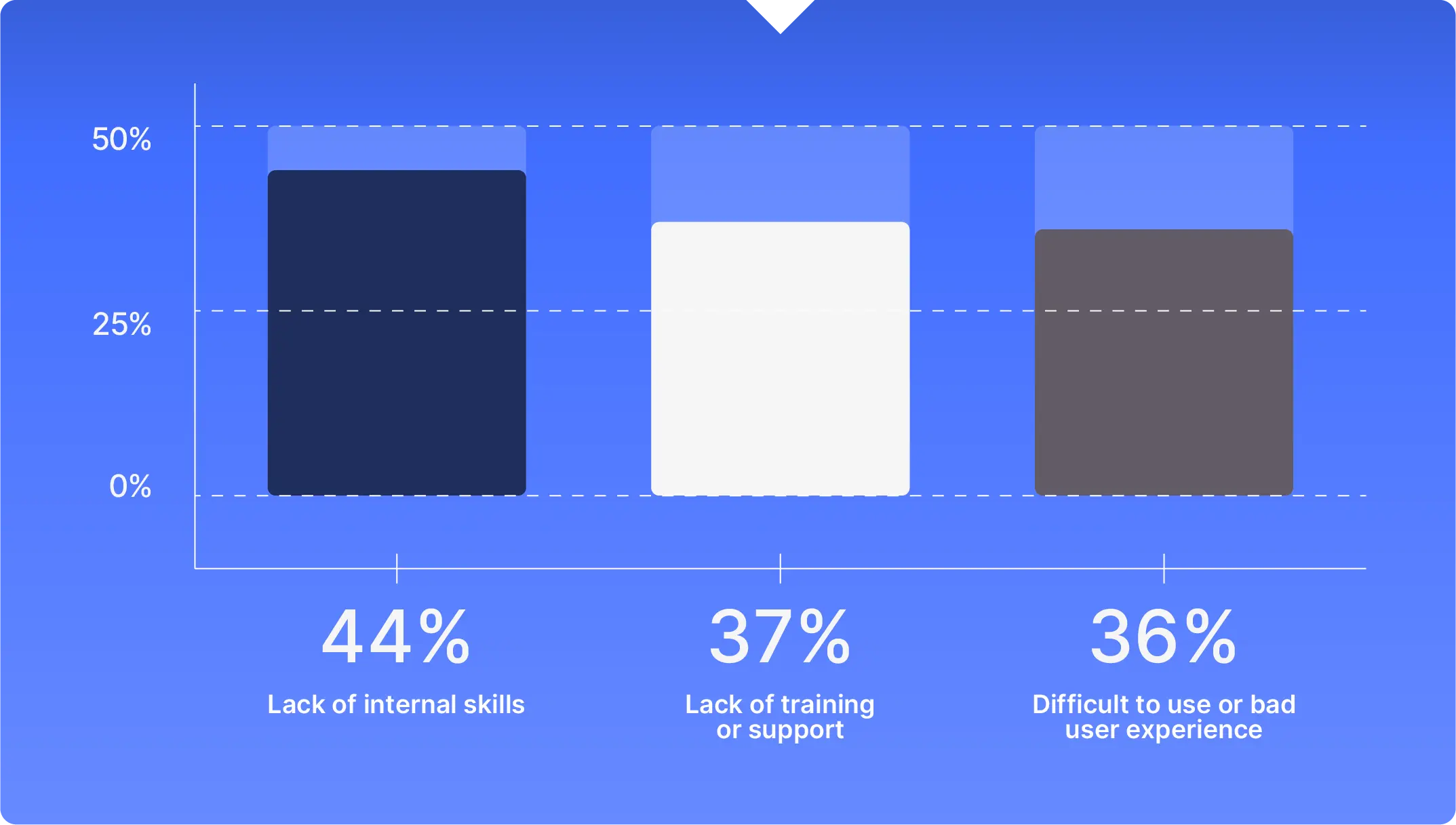

Why does this happen? The top factors identified were:

Some teams simply don’t know how to use all the functionality. Other times, the system is bloated or poorly designed, making features impractical. Both issues overlap.

In fact, a third (32%) of respondents listed “too much unused functionality” as a key regret — second only to “training and support”. New software needs the optimum level of features to encourage its use, and ongoing hands-on support is critical to sustaining its adoption.

When finance leaders choose software that overcompensates for growth, the costs are direct: tens of thousands spent annually on unused capabilities. Poor utilisation also drives teams back to DIY processes, such as manually transferring data or relying on spreadsheets for month-end reporting.

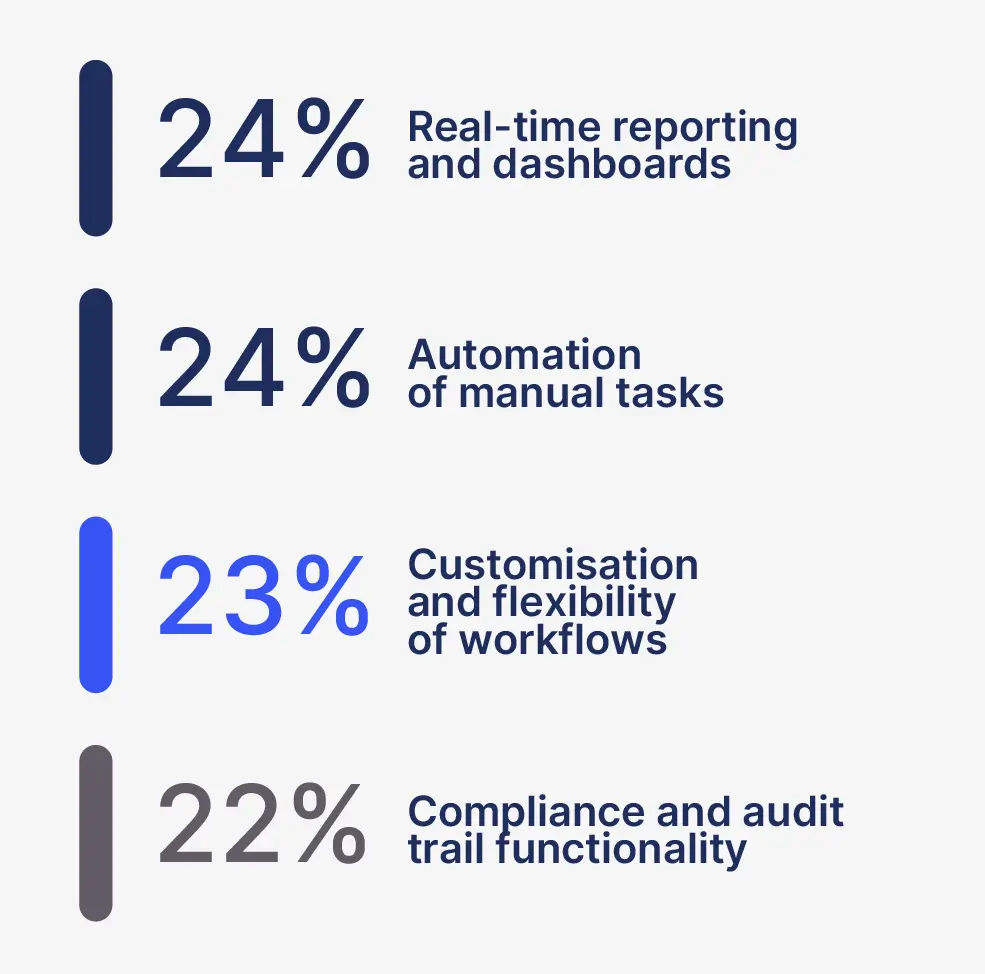

If we take a look at what CFOs are using their finance software for, there is a consistent reliance on different features to support day-to-day work.

When asked to list the top two uses they have for their software, the responses were quite evenly split:

Figures based on multiple answers per respondent

The hidden cost crisis

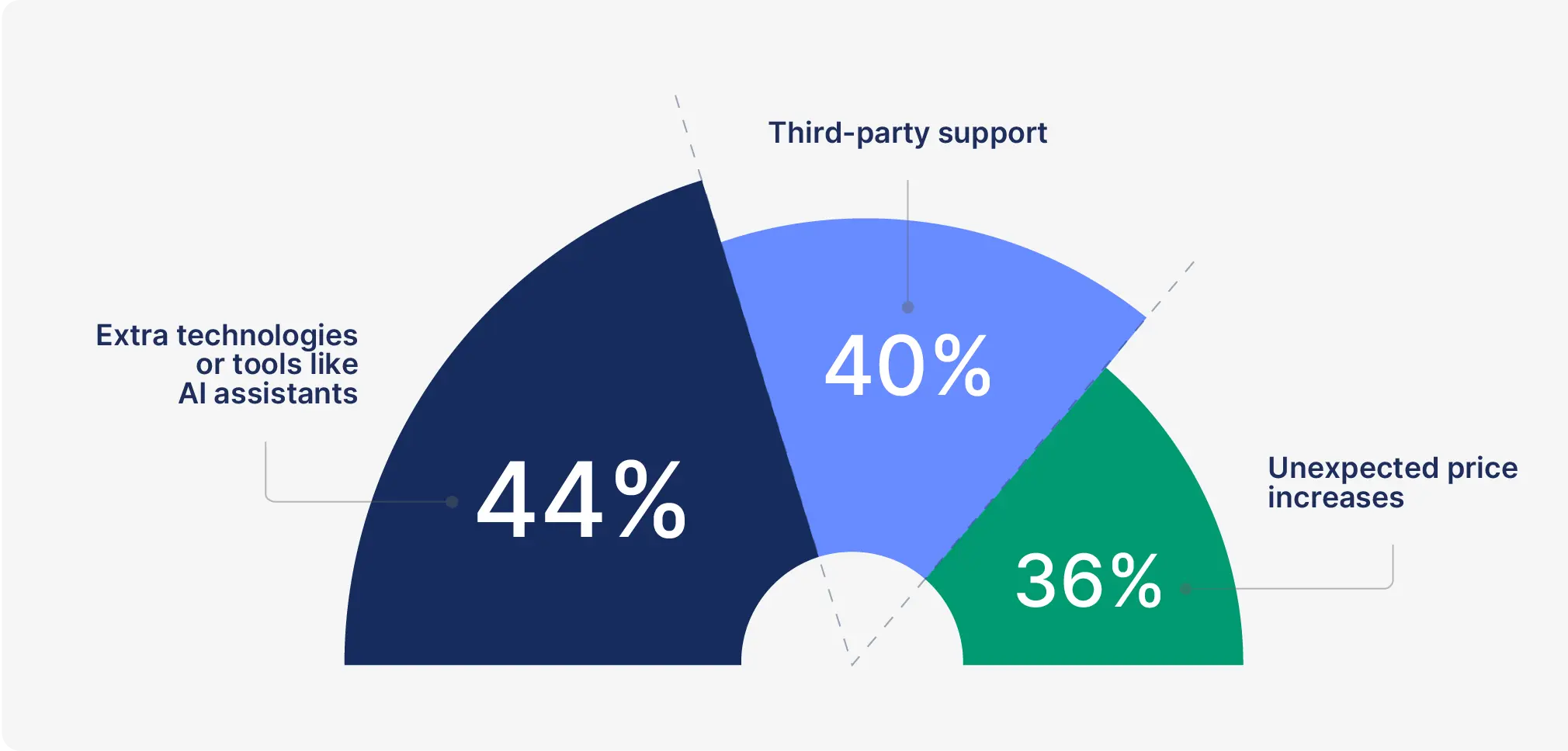

But the deficits don’t stop there. A striking 95% say they have experienced hidden costs with their finance software providers. For more than two in five respondents (41%), these costs were between 50–100% higher than expected.

The top hidden costs cited were:

Scenario 3

You’ve moved into a new office. It looks great, but you soon discover that you have to pay extra to access electricity. Then the rent rises faster and higher than expected. These are costs that weren’t anticipated but are essential features you can’t go without — just like the hidden software fees.

The hunt for better value is driving migrations

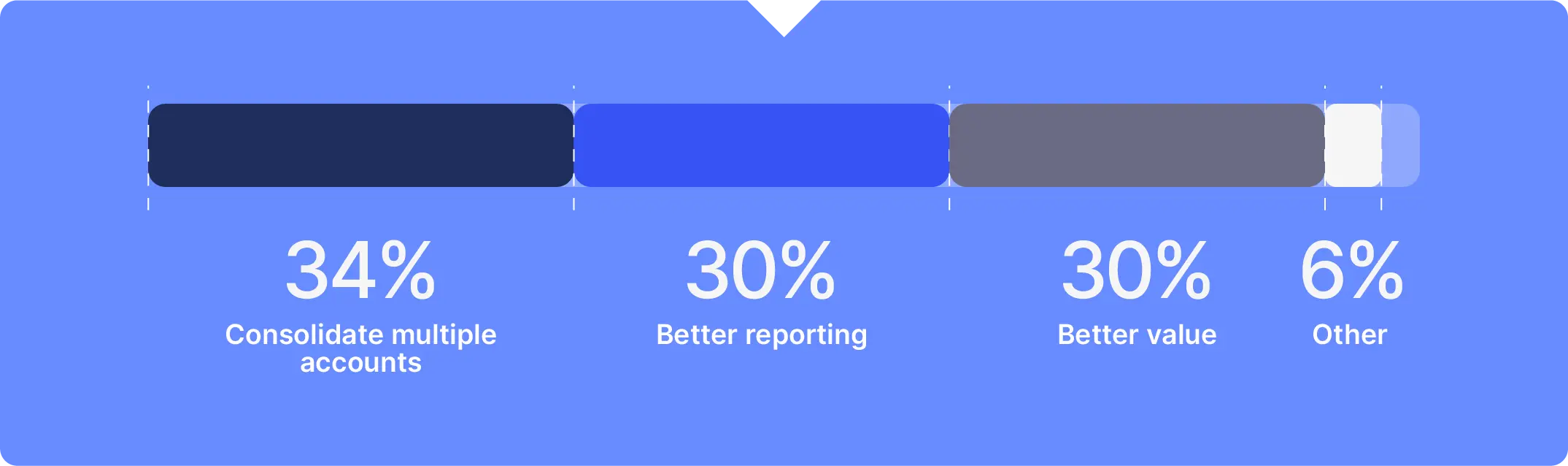

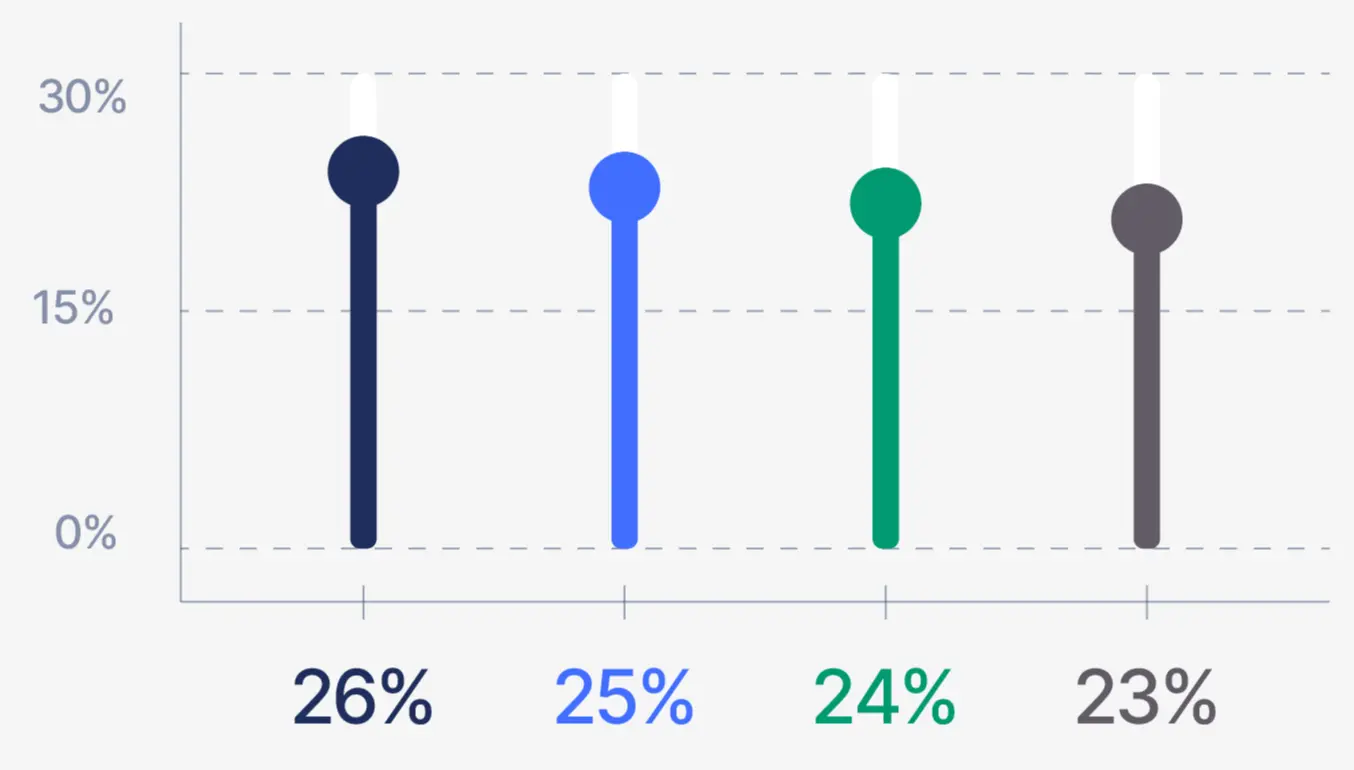

With all of these challenges at play, finance leaders are seeking better-matched software. Some have already found the right fit, but for others, the appeal of switching is growing. Three in every five plan to switch in the next three months!

The vast majority (85%) intend to change within six months — an unusually high short-term migration rate. Their main drivers for making a change are:

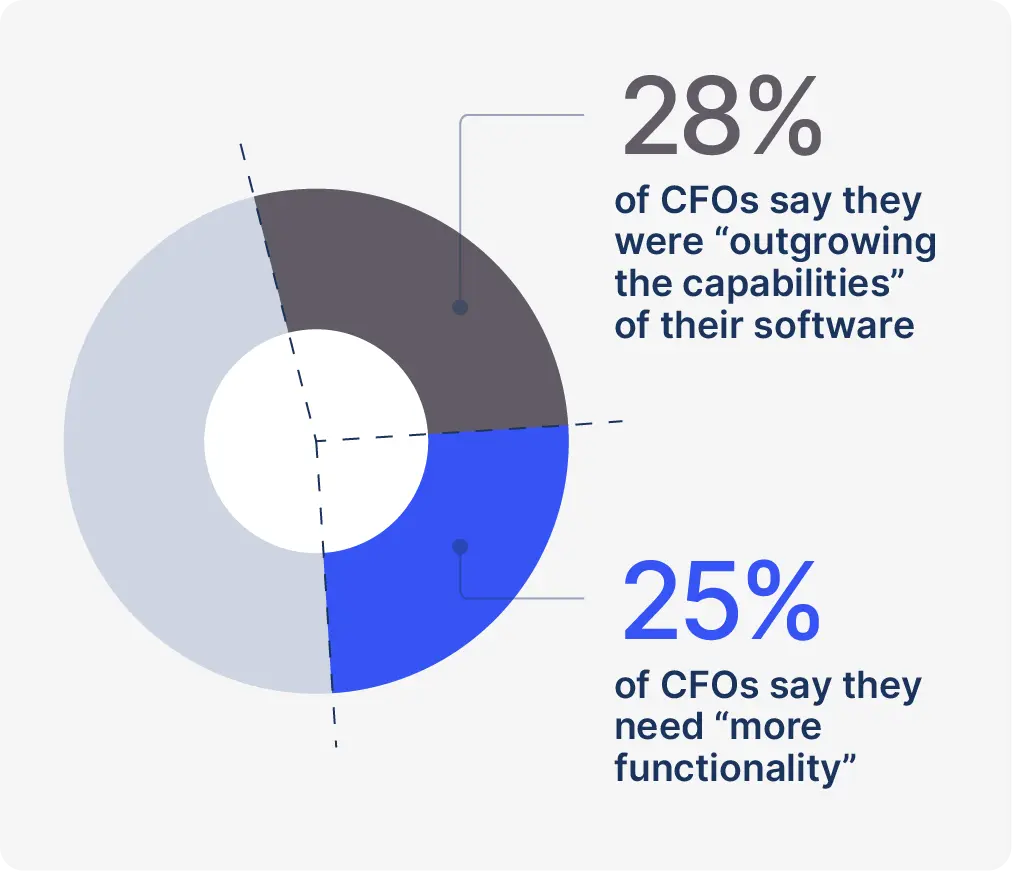

Despite excess features, CFOs say they don’t have the right financial tools for their business. It follows that 28% revealed they were “outgrowing the capabilities” of their current software, while a quarter say they need “more functionality.”

So, they go back to the drawing board and look at what software to choose. But this time, finance leaders can use past pain points to build a stronger, more deliberate approach to how they reach a decision.

The fact that so many CFOs are switching for better consolidation, reporting and value says a lot about where the pain points are. Leaders want tools that give them visibility and control without adding another layer of complexity.”

Chapter 2: The human cost

The work-work balance

The finance profession has long carried a reputation for long hours and a skewed work-life balance. Has this year seen a reset?

In short: No. Almost every CFO, Head of Finance, Financial Controller or Finance Director surveyed said they work weekends or evenings to clear their workload, with 64% saying they do this often or always. Last year, 85% of leaders said they needed an extra 1-2 days a week to clear their work backlog.

The bigger picture is clear: companies are being hit by hidden costs from clunky or overpriced ERP systems, while CFOs and teams pay the human cost — working around the clock and risking burnout to patch inefficient processes.

Inefficient software doesn’t just slow your business down; it eats away at culture. A healthy finance function depends on a healthy working culture.

Scenario 4

A finance professional on £60,000 a year working 8 – 10 unpaid hours weekly is effectively giving £15,000 of overtime annually. For a team of 10, that’s £150,000 in unpaid labour — and 10 extra days worked every week collectively.

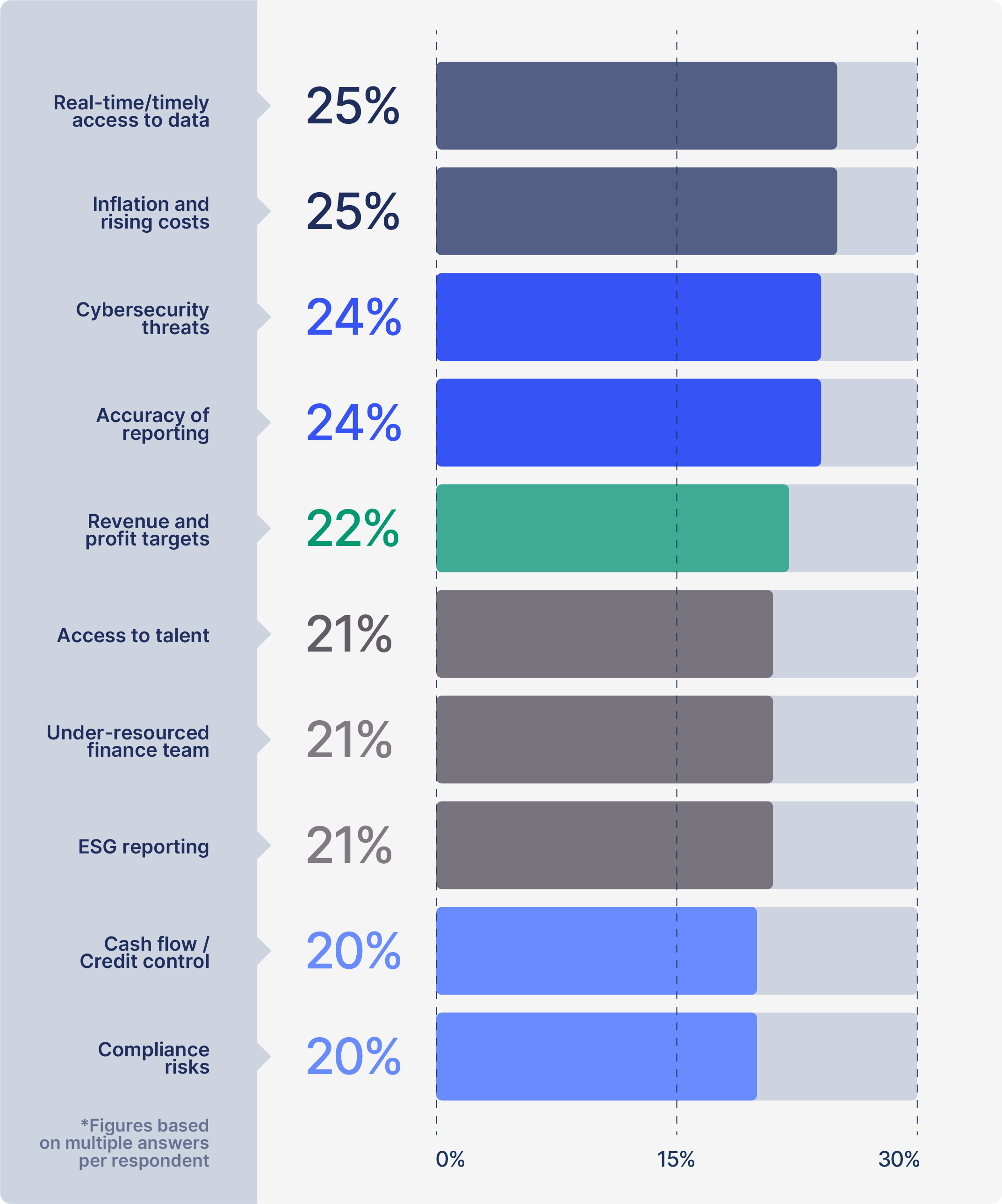

What’s keeping CFOs up at night?

Survey results highlight a mix of internal and external pressures, with timely access to data and rising costs/inflation tied for the top spot (25% each), and cybersecurity close behind (24%).

Notably, concern over access to real-time data has shot up 5% from 20% in last year’s Mindset survey, while inflation and cybersecurity have dropped significantly (from 40% to 25% for inflation and 36% to 24% for cybersecurity). However, this can be attributed to a more even spread of factors concerning leaders, demonstrating that worries are appearing from all angles.

When asked to select the challenges that keep them up at night, the respondents selected a number of topics. What's clear is they are facing a wide spectrum of challenges, with no one issue standing out. This indicates complexity and competing priorities.

If there was ever an illustration of the various demands placed on the modern CFO, this is it.

External economic pressures and cyberattacks present a constant threat to operations.

There is the internal pressure to accurately report on financial performance, meet revenue targets and maintain cash flow, but teams are stretched and access to talent is harder to come by.

And growing responsibilities like ESG reporting are adding to the CFO in-tray.

Expense software is often an obstacle to business success.

It’s a highly unpredictable landscape, but this unpredictability is now a given. Contending with so many concerns, CFOs are recognising that real-time data is the key to helping them navigate internal and external pressures and make informed financial decisions. The ability to access this data underpins how efficiently they can work, how much visibility they have across the company and its entities, and, crucially, how they can guide business strategy.

We weren’t happy with the reporting capabilities in our previous finance system. Every time we wanted a report that wasn’t standard, such as comparing actuals to budget with variances, we had to pay extra. That was on top of an already high annual fee."

Data gaps and decision-making

It’s not just about reporting on figures — it’s about leadership. By shoring up their internal capabilities, finance leaders can ensure their finance function can thrive regardless of external conditions. However:

This lack of consistent, data-driven decision-making limits their ability to improve the company’s financial health, streamline processes, and influence wider strategy.

This statistic is, however, an improvement on last year, suggesting progress. But given the array of concerns, hefty workloads and software challenges, questions remain: what quality of data are finance teams accessing? How effectively is it shared? And how much time is wasted manually extracting and deciphering it?

I've spoken with finance leaders who endured months, sometimes over a year, of resource-draining deployments that left teams stretched thin and morale depleted.

One story that sticks with me is of a finance leader who went into early labour due to the stress of an ERP rollout, and still brought her laptop to the hospital. When she returned from maternity leave, the implementation still wasn’t complete, and the costs had ballooned.”

Chapter 3: Breaking the cycle

What ‘great’ looks like

We’ve seen how choosing the wrong software creates hidden costs: laborious implementations, low utilisation and poor value that send CFOs back to the drawing board.

We’ve also seen how inefficient software and limited real-time data weigh on people: burnt-out teams, uninformed decisions and inefficient functions.

But now, let’s flip it. How can CFOs and finance leaders break the cycle, choose the right finance software and use it as a driver of growth?

Making the decision

When it comes to choosing a finance platform, the main drivers for leaving a software provider (as outlined in chapter one) are also features to look out for:

Different organisations have different requirements. Some wrestle with bloated ERP systems; others outgrow their entry-level tools. But these three gaps are common across both groups, and point to a need for strong mid-tier solutions.

Done correctly, with the right team and platform, implementation can be rolled out in just 4-6 weeks. There should also be non-negotiables. Here are six priorities that emerged in the survey:

support (not through

an outsourced third party)

platforms and bank accounts

and reporting

paying for unused features!)

If you can outline a detailed needs analysis from the outset, with a specific list of key factors and requirements, then you can focus your search on the best solutions for you.

It can be useful to evaluate both what needs to change for your finance team and what has changed for your business. For instance, have you noticed a need to automate manual data entry and re-entry tasks? Is system complexity leading teams to form manual workarounds for tasks like month-end reporting?

Are you now operating across territories and need to consolidate accounts with different currencies? Does your reporting require more dimensions and the ability to drill down on specific KPIs and performance data? What integrations do you need and are any of those requirements complex and need expert support? Understanding these requirements will put you on the right path for choosing your software.”

The golden middle ground: Control and motivation

So, the decision has been made. You’ve chosen software aligned to your needs and size. Implementation has gone smoothly and efficiently. The platform is now up and running. What should that feel like?

Processes

Finance leaders feel more in control: better insights, visibility, and workflows. Instead of chasing manual tasks, they can access live data across entities and provide accurate, timely reporting to stakeholders. Finance processes become smarter, leaner, and more agile.

Strategy

Freed from tedious admin, leaders can focus on scenario planning, forecasting, analysis, and decision-making — building resilience and competitive edge.

Culture

With resourcing a repeated concern, time can also be invested in team development, upskilling, and exploring new tools like AI. Crucially, teams gain a better work-life balance, feel energised, and contribute to a confident, high-performing culture.

Now we’ve switched to AccountsIQ, I’d say it takes about one tenth of the time we’re used to in Sage 50, and you don’t have to worry about the system crashing and corrupting your data!

Running reports now is quick and intuitive and we’ve got the capability to do multi-dimensional reporting, which is incredibly valuable to us.”

AI and future-proofing your company

It’s telling we’ve come this far without mentioning AI. Its role is undeniable, but effective adoption depends on getting core software right first.

When asked what they believe will drive the most change in the finance function by 2030, finance leaders said:

AI and automation

Regulatory changes

Shifts in global

economic power

Decentralised

finance and

blockchain

AI leads, but the even spread shows CFOs expect multiple disruptions.

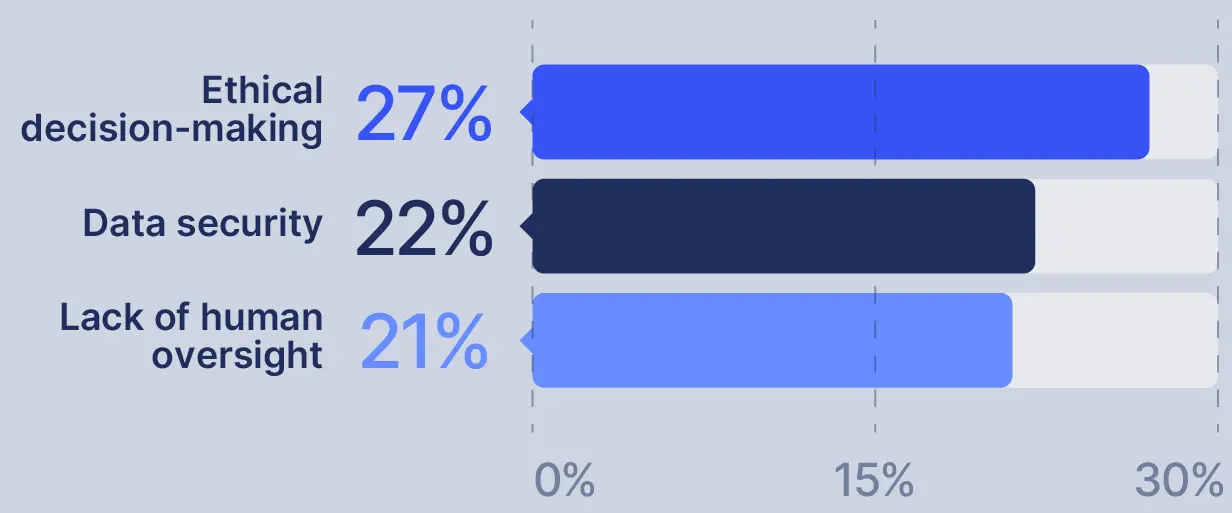

Fears of job losses from AI continue to fall — 13% this year, down from 24% two years ago — signalling growing acceptance of AI as an enabler. Top concerns now focus on its application:

AI is advancing quickly, but its practical use in finance is still being worked out, as businesses and finance teams get to grips on how best to harness its potential. AI tools are only as good as the data they can access, and their eventual value rests on having finance software that can integrate with various platforms and collate data from across the organisation.

Regarding finance processes, we’ll see AI play an increasingly transformative role in activities like information retrieval, reporting and cash flow forecasting.

External regulators like the FCA will be looking to see how firms are using AI and will also expect them to be adopting better financial tools to remain compliant. The EU AI Act is setting a clear direction on how this can be achieved, while the UK has yet to publish its own framework. This makes terminology such as ‘system of record’ and ‘finance ledger’ especially important, along with the safe and explainable use of algorithms, to avoid the risks of the so-called ‘AI black box’, where the decision making process is opaque and difficult to understand.

Easier wins in AI are already emerging where narrow use cases – like alerts or task automation – can apply simple machine learning safely within defined user roles. This helps identify any anomalies or streamline repetitive tasks which usually involve the use of multiple clicks or stages.

Ultimately, businesses need to focus on future-proofing their operations, by implementing software that can scale, integrate AI responsibly and adapt to shifting demands. Equipped with the right tools, CFOs and their teams can move from simply reporting to leading.

What’s next? The route to better

Choosing the wrong finance software carries hidden costs — wasted functionality, long implementations that drain momentum, and a very real toll on finance teams.

The challenge is that mid-sized organisations often feel trapped between starter software and ERPs. But bigger doesn’t always mean better.

As James Hunter, CFO at AccountsIQ puts it: “You don’t need a sledgehammer to crack a nut. Take the time to understand exactly what your finance team needs, and then find a purpose-built finance management system that meets those needs.”

For the finance teams stuck using starter software and looking to upgrade, ERPs don’t have to be the only viable option. And for those already in ERP regret, moving to mid-tier software isn’t wasted investment — it’s a chance to scale more smoothly, remodel processes and avoid paying for functionality you’ll never use.

Ultimately, software isn’t just a tech decision. In today’s unpredictable market, it’s a growth imperative; one that can give finance leaders the clarity and control they need to steer the whole business forward.

CFO Mindset series from AccountsIQ

In 2024, we focused on the lack of control CFOs were feeling. In this second report, we delve into what's driving them to make specific software choices and explore the consequences of these decisions.

These reports form an ongoing series, where AccountsIQ will survey finance leaders to benchmark ongoing sentiment and explore the key issues that matter most to mid-market finance teams.

Don't wait for the next report!

Features

Compare

Support

Company